As first mentioned in part 1 of this three-part blog series, the rise in financial technology (FinTech) firms is having a disruptive impact on today’s banks, threatening their customer base and revenue through the launch of new digital services. CGI conducted a survey in 2016 to help gauge this impact, reaching out to bank consumers to explore their expectations and assess how banks can better compete with FinTechs in meeting those expectations.

We surveyed 1,670 consumers across eight countries to get their perspectives on 12 digital FinTech services:

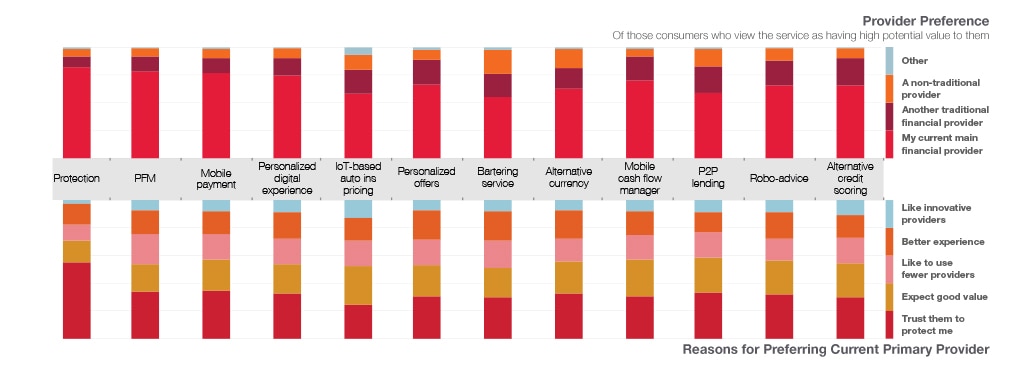

- Protection

- Personal finance management (PFM)

- Mobile payments

- Personalized digital experience

- IoT-based auto insurance pricing

- Personalized offers

- Bartering

- Alternative currency

- Mobile cash flow manager

- P2P lending

- Robo-advice

- Alternative credit scoring

The survey assessed the value consumers place on these services, along with their awareness and usage of them. It also explored obstacles that hinder their purchasing, and asked what type of provider they prefer and why.

In the first blog, I cover what services consumers value the most, along with their service awareness and usage. This second blog discusses their purchasing obstacles and provider preferences, and I’ll be sharing a third blog with key recommendations for both banks and FinTechs.

Purchasing obstacles

The results of our survey show that the biggest purchase impediment for all 12 digital services is a lack of trust among consumers. Consumers lack trust in the companies that provide these services (largely FinTechs) due to their newness in the market and divergence away from traditional banking. In addition, consumers have trust issues when it comes to providing the personal data these services require.

This trust gap shows how important it is for new entrants to find ways to establish trust or alternatively leverage (e.g., through partnerships) trust that has already been established through incumbent providers.

Complexity is another obstacle. Many consumers believe these new digital services are too complex or the application process is too difficult. This complexity can be attributed both to poor service design and/or the lack of a clearly communicated value proposition.

Finally, many consumers are simply risk averse. They’d rather let others test the waters in trying out new services and providers before taking the risk themselves.

Interestingly, price is not a major obstacle at this point in time. This reflects the relatively low entry-level pricing for new digital services and the fact that consumers are more concerned about core issues such as trust.

Provider preferences

The survey delivers good news for banks and a warning for FinTechs in terms of service provider preferences among consumers. Results show that consumers overwhelmingly prefer to receive new digital services from their current primary financial institution, mainly because of trust. Behind current providers, other traditional providers came in second, followed by nontraditional providers at a distant third.

This demonstrates that established banks have a great opportunity to expand customer relationships by offering new digital services, and, that those banks that do not move quickly run the risk of consumers going elsewhere, i.e., turning to other banks or directly to FinTech firms.

For FinTechs, it’s clear that getting access to customers is a major challenge. While a few additional players may succeed with a “go it alone” strategy, the majority of FinTechs that succeed will likely overcome this hurdle by partnering with incumbent banks.

In our final blog in this series, we’ll share some recommendations for both banks and FinTechs in light of the survey’s findings. In the meantime, feel free to download our survey, “FinTech Disruption in Financial Services,” or contact me with any questions.

About this author

Kevin Poe

Vice-President, Consulting Expert

Kevin Poe leads CGI’s U. S. financial services consulting practice, which provides a wide range of services related to strategy, operations, and execution. Prior to his current role, Kevin oversaw CGI’s Financial and Insurance Solutions Group, which encompasses CGI’s software solutions in credit management, payments, ...