Today’s banks are facing a number of unprecedented challenges, including the rise in financial technology (FinTech) firms. These innovative startups are focused on taking a share of bank customers, products and revenues through new digital services, and staying ahead of them is high on banks’ agendas. In the face of FinTech disruption, CGI set out to capture the voice of the consumer. What do consumers want, and how can banks out compete the FinTechs in meeting their expectations?

In 2016, we surveyed 1,670 consumers across the U.S., Canada, the UK, France, Germany, Sweden, Singapore and Australia to get their perspectives on 12 digital FinTech services such as peer-to-peer (P2P) lending, mobile payments and robo-advice. Our survey examined the following:

- Value placed on these services by consumers

- Consumer awareness and usage

- Purchasing obstacles

- Provider preferences and influencers

In this three-part blog series, we’ll cover the survey’s key findings and provide recommendations for how banks should respond. This first blog addresses what services consumers value the most, along with their service awareness and usage. In the second blog, we’ll discuss their purchasing obstacles and provider preferences. And, in the last blog, we’ll share a few key recommendations for banks.

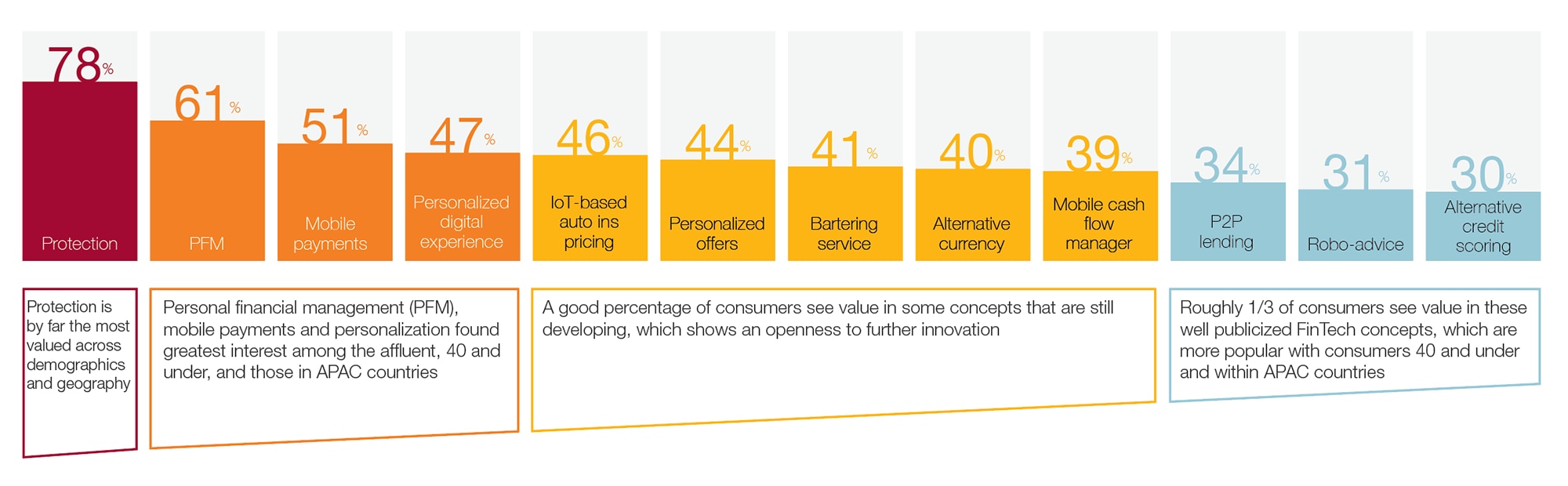

Most valued services

The 12 digital services analyzed by the survey include the following: protection, personal finance management (PFM), mobile payments, personalized digital experience, IoT-based auto insurance pricing, personalized offers, bartering, alternative currency, mobile cash flow manager, P2P lending, robo-advice, and alternative credit scoring.

Of these, protection is by far the most valued digital service across all demographic groups and countries. This finding is not surprising in light of growing consumer concerns about cyber attacks, identity fraud and other security risks.

The next most valued services are personal financial management, mobile payments and personalization. Preference for these services indicates consumers’ increasing desire for convenience and digitization of the banking experience—the same type of experience they enjoy from retailers.

Interestingly, digital services that are getting the most media attention, including P2P lending, robo-advice and alternative credit scoring, are the least valued services by surveyed consumers. Only about one-third of respondents, mainly consumers 40 and under, see value in these well-publicized services.

Percentage of consumers who value each service

Awareness and usage

In terms of consumer awareness, mobile payments are the most broadly known service (94%), followed by protection, personalization and P2P lending. However, the survey found a significant gap between awareness and intended use of a service, with only 33% reporting current or planned use. This gap is highest for P2P lending, with a drop from 75% in awareness to only 25% intended use among consumers who see value in it. Close behind is robo-advice, with a drop from 68% in awareness to 24% intended use.

These large gaps between awareness and expected use demonstrate that finance firms have significant work to do to convince even interested consumers to move from awareness to consideration to purchase. And, this calls for a closer look at the obstacles holding back these interested consumers, which will be the topic of our next blog. We’ll take a look at some of the biggest purchasing obstacles and also explore provider preferences and influencers among consumers.

Until then, download our survey, “FinTech Disruption in Financial Services.” Also, feel free to reach out to me with any questions you might have.

About this author

Kevin Poe

Vice-President, Consulting Expert

Kevin Poe leads CGI’s U. S. financial services consulting practice, which provides a wide range of services related to strategy, operations, and execution. Prior to his current role, Kevin oversaw CGI’s Financial and Insurance Solutions Group, which encompasses CGI’s software solutions in credit management, payments, ...